Login

Login

Go Back to blog listing page

Go Back to blog listing page

50 Lakh Home Loan EMI: Interest Rates, Tenure, and Eligibility Criteria

October 30, 2024

1 min

A home loan is a significant financial commitment and understanding the associated costs is crucial. One of the most important factors to consider is the equated monthly instalment (EMI). In this article, you will learn everything you need to know about a 50 lakh home loan EMI, including home loan interest rates, tenure, and eligibility criteria.

What is an EMI?

An EMI is the fixed monthly payment you make to repay your home loan over a chosen tenure. Each EMI consists of two components — the principal amount (the loan amount itself) and the interest accrued on the loan. In the initial stages, a larger portion of the EMI goes toward the interest, and as the loan progresses, more goes toward repaying the principal. This repayment structure is designed to ease the borrower with manageable monthly payments over time.

Several factors influence your EMI:

- Interest Rate: The higher the interest rate, the higher your EMI.

- Loan Amount: A larger loan amount will result in higher EMIs.

- Loan Tenure: A longer loan tenure can lead to lower EMIs but higher overall interest costs.

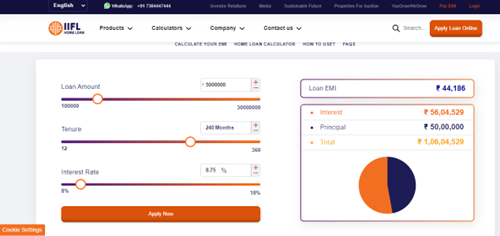

Calculating your EMI online

With the advent of online tools, calculating your EMI has never been easier. Home loan EMI calculators provided by banks and financial institutions allow you to input your loan amount, interest rate, and tenure to instantly see what your monthly installment will be. The 50 lakh home loan EMI calculators help you visualize how different variables like tenure and interest rates affect your EMI so that you can make an informed decision before taking a loan.

Interest Rates for a ₹50 Lakh Home Loan

Interest rates for home loans fluctuate based on various economic factors. Currently, home loan interest rates in India hover between 8.5-9% for most borrowers, depending on their credit score and the lenders. Keeping an eye on these benchmarks allows borrowers to negotiate better rates or choose the right time to lock in a rate.

Interest rates are often affected due to the following reasons:

- Economic Conditions: The overall economic health and interest rate trends can impact home loan rates.

- Lender Policies: Different lenders have varied pricing strategies and may offer varying home loan interest rates.

- Your Profile: Your credit score, income, and other financial factors can influence the home loan interest rate you're offered.

Depending on your risk-taking capacity, you can choose either a fixed or floating interest rate. Fixed rates remain constant throughout the loan tenure while floating rates can fluctuate based on market benchmarks.

Read more: Fixed and Floating Rate Home Loans: Which Option is Right for You?

Which loan tenure is ideal for you?

The tenure of your home loan of 50 lakh EMI can significantly impact your monthly payments. Longer tenures, such as 20 years, offer lower EMIs, making them affordable every month. However, longer tenures mean higher total interest costs. In contrast, shorter tenures increase your monthly EMI but reduce the total interest paid over the loan’s lifespan, enabling faster debt clearance.

When deciding on loan tenure, it's essential to consider your financial goals and capacity. A 50 lakh home loan EMI for 20 years might be more manageable month-to-month, but if you aim to reduce your total interest paid, a shorter tenure could be beneficial.

You can easily compare EMIs for different loan tenures using a 50 lakh loan EMI calculator. By adjusting the tenure slider, you’ll see how your monthly payments change. The home loan EMI calculator is a great tool for determining the most comfortable EMI for your financial situation without overextending your budget.

Eligibility criteria for a ₹50 lakh Home Loan

To qualify for a 50 lakh home loan, borrowers must meet certain eligibility criteria. Lenders evaluate various factors before approving a loan, ensuring the borrower can manage the 50 lakh loan EMI.

- Income Requirements: Lenders require borrowers to demonstrate a stable income capable of supporting the home loan of 50 lakh EMI. Lenders typically look for a debt-to-income ratio that indicates you can manage the loan repayment without strain. Salaried individuals may need to show consistent earnings over several years, while self-employed applicants may need to provide tax returns and financial statements to prove income stability.

- Credit Score: A healthy credit score is crucial when applying for a home loan. Most lenders prefer a credit score of 750 or above, as it demonstrates a history of responsible credit usage and repayment. A higher credit score not only improves your chances of loan approval but also qualifies you for better home loan interest rates. If your credit score is below the desired level, consider improving it before applying for a loan by clearing outstanding debts and maintaining timely payments.

- Documentation: To process your home loan, lenders will require a variety of documents. These typically include identity proof (like an Aadhaar card or passport), income proof (salary slips or tax returns), bank statements, property documents, and employment details. Ensuring that you have all these papers ready can speed up the loan approval process.

- Other Factors: Apart from income and credit score, lenders also evaluate factors like your employment stability and the value and location of the property. Stable employment in a reputable company or steady business income can enhance your eligibility. The property's location and market value also play a role, as lenders assess the resale potential and security of their investment.

Wrapping Up

Obtaining a 50 lakh home loan requires careful planning and consideration of various factors. By understanding interest rates, loan tenure, and eligibility criteria, you can make an informed decision and secure a loan that aligns with your financial goals. For more information and expert guidance on home loans, explore IIFL Home Loans.

Tags

Most Read Blogs

Frequently Asked Questions (FAQ’s)

Q1. Can I prepay my home loan before the end of the tenure?

Ans:

You can prepay your home loan before the end of its tenure, but some lenders might impose prepayment penalties.

Q2. Can I apply for a joint home loan of 50 Lakh?

Ans:

Yes, applying for a joint home loan can enhance your eligibility, as combined incomes allow for higher loan amounts and potentially lower EMIs.

Q3. Is it better to choose a fixed or floating rate for a home loan?

Ans:

Fixed rates offer stability while floating rates provide potential savings when market rates drop. The choice depends on your financial goals.

Q4. What happens if my credit score is low?

Ans:

A low credit score may lead to higher interest rates or even loan rejection. Improving your credit score before applying is advisable.

Q5. What is the maximum tenure for a ₹50 lakh home loan?

Ans:

Most lenders offer home loan tenures of up to 30 years, depending on your eligibility such as age, income, credit score, employment stability, and existing financial obligations. Lenders assess these factors to determine your ability to repay the loan.

What can we help you with?

Home Loan

Secured Business Loan

Balance Transfer

Home Improvement Loan

Home Loan for Uniformed Services

NRI Home Loan

Home Loan

Secured Business Loan

Balance Transfer

Home Improvement Loan

Home Loan for Uniformed Services

Get instant support with existing loan related queries

Raise a Request Get instant access to your existing Loan Account with us Raise a Ticket

Call Helpline Speak with our Customer Support Executive on 1860 267 3000

Visit Nearby Branch You can walk into any of our 300+ branches, spanning across 18 states Get Directions

Our Brands & Subsidiaries

Insurance Partners

HDFC Life Insurance

Learn more

Bajaj Life Insurance

Learn more

ICICI Prudential Life Insurance

Learn more

Go Digit General Insurance

Learn more

Aditya Birla Capital Insurance

Learn more

Bajaj Allianz General Insurance

Learn more