Login

Login

Go Back to blog listing page

Go Back to blog listing page

Why you should consider a Balance Transfer for lower interest rates in 2025?

February 28, 2025

1 min

A home loan is a long-term financial commitment, and even a small reduction in interest rates can lead to significant savings. With interest rates fluctuating and lenders offering competitive deals, a home loan balance transfer has become a feasible option for borrowers looking to reduce their financial burden.

By transferring your loan to another lender offering lower rates and better terms, you can ease your repayment journey while maximizing savings. But is it the right move for you? Let’s break it down.

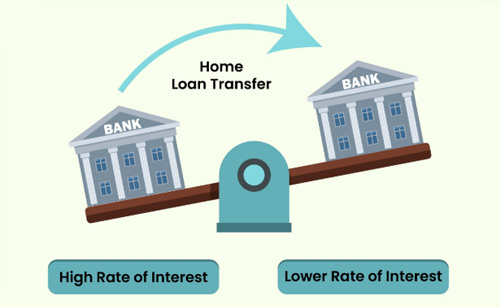

What is a Home Loan Balance Transfer?

A home loan balance transfer allows borrowers to shift their existing loan from one financial institution to another that offers less interest rate for home loans, better terms, or enhanced benefits. This transfer ensures you pay less interest over time, making your EMIs more manageable.

In essence, the new lender repays the outstanding amount to your previous lender, and you start making payments to the new lender at a reduced interest rate. The process is beneficial if your current lender’s terms are no longer favorable or if another financial institution provides better features such as top-up loans or flexible repayment options.

Why opt for a Home Loan Balance Transfer

A home loan balance transfer is not just about securing the lowest housing loan interest rates. It comes with multiple advantages that can improve your financial stability. Here are a few compelling reasons to consider transferring your home loan:

- Lower interest rates: One of the primary reasons borrowers opt for an HLBT is to get low interest home mortgage loans, which can lower monthly EMIs significantly.

- Better loan terms: Some lenders offer flexible repayment tenures, helping you choose an EMI structure that aligns with your financial goals.

- Reduced EMI burden: A lower interest rate directly impacts your EMI, allowing you to save more each month.

- Top-up loan facility: Many financial institutions provide additional funds in the form of a top-up loan, which can be used for home renovation, education, or other financial needs.

- Improved customer service: If you're dissatisfied with your current lender’s service, switching to a more customer-friendly institution can enhance your overall experience.

- No prepayment penalty on floating rate loans: According to RBI guidelines, banks and NBFCs cannot charge prepayment penalties on floating-rate home loans, making the transfer process more cost-effective.

Costs involved in Home Loan Balance Transfer

While the benefits of a balance transfer are appealing, it is essential to factor in the associated costs before making a decision.

- Processing fee

Most lenders charge a processing fee (typically 0.5%–1% of the loan amount) when approving the transfer. Some lenders may waive this charge as a promotional offer. - Prepayment charges (If applicable)

Though RBI has mandated that no prepayment penalty should be charged on floating-rate loans, some fixed-rate home loans may still attract foreclosure charges. - Legal and administrative fees

Lenders might charge legal verification fees, valuation fees, and stamp duty costs while processing your loan transfer. These charges vary across institutions. - Balance transfer evaluation cost

Your new lender will conduct a thorough assessment of your financial profile and the property before approving the transfer, which may involve additional verification charges. - Top-up loan charges

If you avail of a top-up loan during the transfer, it may come with its own set of charges, including documentation and processing fees.

Home Loan Balance Transfer Process

The process of transferring your home loan to a new lender involves multiple steps. Here’s how you can go about it:

- Step 1: Check your current loan details

Before applying for a transfer, review your outstanding loan amount, interest rate, and tenure. Also, check if your current lender has any prepayment or foreclosure charges. - Step 2: Compare lenders and interest rates

Research different lenders and compare interest rates, processing fees, and benefits. Choose a lender that offers the best deal with minimum costs. - Step 3: Submit a balance transfer request

Apply to your existing lender for a loan closure letter and a No Objection Certificate (NOC). This document confirms that your loan is being transferred. - Step 4: Apply with the new lender

Submit your application along with the required documents like:- Loan closure letter and NOC

- Identity and address proof

- Income proof (salary slips, IT returns, etc.)

- Property-related documents

- Loan account statement

- Step 5: Loan approval & new agreement signing

Once the new lender approves your application, they will disburse the amount to your old lender, closing your previous loan. You’ll then sign a fresh loan agreement with new terms. - Step 6: EMI payments with a new lender

After the successful transfer, your EMI payments will continue with the new lender as per the agreed terms.

Final Thoughts

A home loan balance transfer can be a game-changer for borrowers looking to lower their interest burden and enhance financial flexibility. However, it’s important to evaluate the savings against transfer costs before making the switch. If done strategically with experts at IIFL Home Loans, a balance transfer can lead to substantial financial gains while offering better repayment terms.

Tags

Most Read Blogs

Frequently Asked Questions (FAQ’s)

Q1. When should I opt for a home loan balance transfer?

Ans:

You should consider a balance transfer when a new lender offers significantly low-interest home mortgage loans, better loan terms, or additional benefits such as a top-up loan.

Q2. Is there a limit on the number of times I can transfer my home loan?

Ans:

There is no limit, but frequent transfers can attract processing fees and impact your credit score. It’s advisable to switch only when there is a clear financial advantage.

Q3. Will my credit score be affected if I transfer my home loan?

Ans:

A balance transfer does not negatively impact your credit score as long as you continue making timely EMI payments. However, multiple loan inquiries can have a minor impact.

Q4. How much can I save with a home loan balance transfer?

Ans:

The exact savings depend on the difference in interest rates, outstanding loan amount, and tenure. Use a home loan balance transfer calculator to estimate your potential savings.

Q5. Can I avail of a top-up loan during a balance transfer?

Ans:

Yes, many lenders offer top-up loans along with balance transfers, allowing borrowers to access additional funds at attractive interest rates.